Renewable energy sources are set to represent almost three quarters of the $10.2 trillion the world will invest in new power generating technology until 2040, thanks to rapidly falling costs for solar and wind power, and a growing role for batteries, including electric vehicle batteries, in balancing supply and demand.

- Wind and solar make up almost 50% of world electricity in 2050 – “50 by 50” – and help put the power sector on track for 2 degrees to at least 2030

- A 12TW expansion of generating capacity requires about $13.3 trillion of new investment between now and 2050 – 77% of which goes to renewables.

- Europe decarbonizes furthest, fastest. Coal-heavy China and gas-heavy U.S. play catch-up.

- Wind and solar are now cheapest across more than two-thirds of the world. By 2030 they undercut commissioned coal and gas almost everywhere.

- Batteries and flexibility bolster the reach of renewables: Utility-scale batteries increasingly compete with natural gas to provide system flexibility at times of peak demand. In conjunction with small-scale batteries, this will help renewable energy reach 74% penetration in Germany, 38% in the U.S., 55% in China and 49% in India by 2040.

- Electric vehicles bolster electricity use: In Europe and the U.S., EVs will account for 13% and 12% of electricity demand by 2040. Charging EVs flexibly, when renewables are generating and wholesale prices are low, will help the system adapt to intermittent solar and wind.

- Consumer energy decisions such as rooftop solar and behind-the-meter batteries help shape an increasingly decentralized grid the world over.

- Batteries, gas peakers and dynamic demand help wind and solar reach more than 80% penetration in some markets..

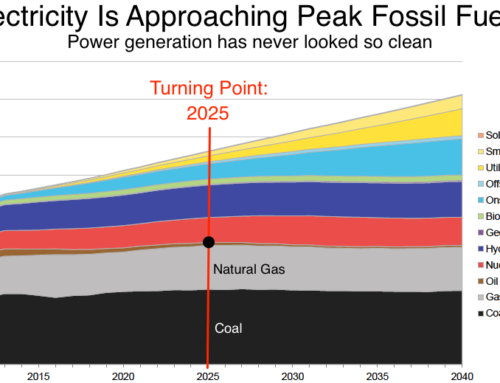

- Coal continues to grow in Asia, but collapses everywhere else and peaks globally in 2026.

- Gas-fired power grows just 0.6% per year to 2050, supplying system back-up and flexibility rather than bulk electricity in most markets.

- Making heat and transport electric lowers emissions. The challenge is scale.

- To keep an electrified energy sector on a 2-degree trajectory, we will need to deploy additional zero-carbon technologies that are dispatchable and economic running at low capacity factors, or technology that can capture and sequester emissions at scale.

Read further on https://about.bnef.com/new-energy-outlook/?src=learn1?